By the end of this month, the Internal Revenue Service will have received about 140 million individual tax returns. Many of those who have filed this year will have hoped to see greater tax relief than they have years past. The tax legislation passed by Congress in December 2017 promised to lower the tax burden for a large swath of American households. One way it does this is by doubling the standard deduction—the baseline deduction in taxable income every taxpayer is eligible to take. Taxpayers are celebrating the change, but charitable organizations are decidedly less enthusiastic about it.

By the end of this month, the Internal Revenue Service will have received about 140 million individual tax returns. Many of those who have filed this year will have hoped to see greater tax relief than they have years past. The tax legislation passed by Congress in December 2017 promised to lower the tax burden for a large swath of American households. One way it does this is by doubling the standard deduction—the baseline deduction in taxable income every taxpayer is eligible to take. Taxpayers are celebrating the change, but charitable organizations are decidedly less enthusiastic about it.

Charities are aggrieved because a larger standard deduction will likely reduce the number of taxpayers who itemize their deductions (rather than take the standard deduction) —and the number of taxpayers who take the tax deduction for charitable contributions (which I refer to as the charitable deduction). The charitable deduction is only available to itemizers, currently about a third of taxpayers. It works by lessening the cost of charitable gifts proportionally by one’s marginal income tax rate; i.e., the after-tax cost of charitable gifts declines as one’s income bracket increases. Now that the standard deduction has doubled in size, some taxpayers who itemized in years past will likely take the standard deduction this year and will no longer have a tax-related motivation for making donations.

This means we might see a dip in charitable giving. Charities have not hesitated to register their displeasure about this. As the tax legislation began to take form last fall, charities began to express their concerns that a diminished itemizer class would strip them of their ability to meet basic needs. In a statement to New York Times columnist Ann Carns, Feeding America executive Diana Aviv explained how a potential decline in charitable giving would “devastate [their] ability to provide food assistance;” Orvin Kimbrough of the United Way of Greater St. Louis voiced his concerns in similarly stark terms: “This is about people’s lives.”

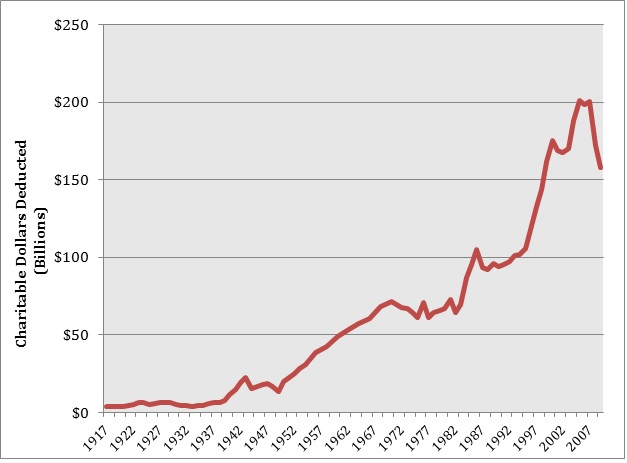

The recent tax legislation is the hot button issue of the moment, but charities’ concern with the charitable deduction dates back generations. The charitable deduction is one of the oldest deductions in the tax code. It has been in place since 1917, and charitable organizations have been the policy’s primary lobbying constituency for nearly as long. Over the years, the charitable deduction has grown from a small tax break for a high-taxpaying elite—when the legislation was originally passed in 1917, marginal income tax rates had peaked at above 70 percent—to one of the nation’s ten largest tax expenditures. The deduction’s size in terms of charitable dollars deducted has skyrocketed from $4 billion in inflation-adjusted dollars in 1917 to over $200 billion today (Figure 1). And charitable organizations have nurtured this prodigious growth, collectively mobilizing to protect and expand the charitable deduction in moments of political contestation.

Figure 1 – Inflation-adjusted Deduction Size in Raw Dollars Deducted, 1917-2009

Source: Tax Policy Center, “Itemized Charitable Contributions, Total Amount, Percentage of Percentage of AGI, and Percent of GDP, 1917–2009.”

On the face of it, charities’ support of a tax deduction that incentivizes charitable giving makes perfect sense. But charities’ ardent defenses of the policy have masked its distributive effects—and particularly the outsized benefits it bestows on elites and elite organizations. In fact, elite taxpayers reap the greatest subsidies from the charitable deduction without having to raise their voice in defense of the policy at all.

The charitable deduction was originally created to incentivize elite giving during World War I, when the federal income tax applied only to elites and tax rates had spiked from less than 10 percent to over 70 percent to fund the war. Over time, the structure of the deduction has remained the same, but marginal income tax rates have plummeted and the size and scope of the charitable sector has expanded considerably. By the late twentieth century, peak marginal income tax rates had begun to fall—from over 90 percent in the 1950s to 70 percent in the ‘70s to an all-time low of 28 percent in the Reagan era. Meanwhile, charitable organizations had emerged as a core component of the nation’s welfare apparatus. As the charitable sector has become larger and more legitimate, charities’ mobilization in defense of the deduction has only increased. And because charities are the deduction’s main constituency, they’ve played a major role in shaping the narrative around the policy.

Their narrative rests on the claim that the charitable deduction is a broad social benefit central to the provision of fundamental societal needs. Over the years, charitable organizations have drawn upon different frames to illustrate the importance of the policy, but they have never wavered in their defense of it as a cornerstone social protection. During World War II, charitable organizations promoted the charitable deduction as a reward for those who supported cherished social institutions—especially churches, colleges, and universities, which many saw as central to the American way of life. By the latter half of the twentieth century, and especially during 1980s era of rising anti-state sentiment, charities had come to cast their work as a necessary counterbalance to the public sector, and the charitable deduction came to be seen as an engine for the (much-desired) private provision of public goods. And today, as nonprofit social service provision has become more accepted and visible, charitable organizations have come to describe the deduction as a sanction for their efforts to meet public needs that the government has failed to or chosen not to address. Through it all, they have heralded the deduction as way of helping protect the poor.

As this narrative has taken hold in the political imagination, elites have quietly netted a greater share of the policy’s benefits over time. As top incomes have risen, high earners have taken greater advantage of the policy as a means of sheltering wealth. Consider differences in the proportion of taxpayers taking the charitable deduction between 1990 and 2015, the most recent year in which data are available: In 1990, taxpayers making $1 million or more accounted for 0.2 percent of those taking the deduction, and their charitable dollars made up 9 percent of all dollars deducted. By 2015, $1 million plus earners made up 1 percent of all taxpayers taking the deduction, and their charitable dollars made up 29.8 percent of all dollars deducted. The effect increases as incomes increase: in 2015 those making $10 million or more made up only 0.05 percent of all taxpayers taking the deduction, but they made up a whopping 16.7 percent of all of dollars deducted. This may not be all that problematic if elites were donating large sums to basic needs organizations, but evidence shows that elites give differently than members of the middle and working classes. Elites are much more likely to support elite institutions—foundations, higher education, health, and arts organizations—and far less likely to support social service organizations than their non-elite peers.

Despite these distributive effects, charitable organizations’ narrative about the policy has stuck. Today the charitable deduction receives widespread public support, to the point that many misunderstand how the policy works. Over 70 percent of Americans favor it—and over 50 percent of Americans claim that they benefit from it, even though only a maximum of about 30 percent of taxpayers (those who itemize) actually take the deduction.

The new tax law, and especially the doubling of the standard deduction, may indeed decrease charitable giving as fewer taxpayers itemize than in years past, but it probably won’t do much to change the dynamics described here. Elites will continue to enjoy outsized benefits from the policy and will continue to bestow these benefits on the organizations they care about, the majority of which do comparatively little to support the poor. Meanwhile, charities’ efforts to protect the deduction have insulated it from reform—or even critique.

Read More

Kelly L. Russel, ‘The Politics of Hidden Policy: Feedback Effects and the Charitable Contributions Deduction’, in Politics & Society.

Image: Mike Mozart via Flickr (CC BY 2.0).

Cross-posted at the LSE US Centre’s daily blog on American Politics and Policy.

No Comments