Climate change is making the planet we inhabit a more dangerous place to live. After the devastating 2017 hurricane season in the U.S. and Caribbean, it has become easier, and more frightening, to comprehend what a world of more frequent and severe storms and extreme weather might portend for our families and communities.

Climate change is making the planet we inhabit a more dangerous place to live. After the devastating 2017 hurricane season in the U.S. and Caribbean, it has become easier, and more frightening, to comprehend what a world of more frequent and severe storms and extreme weather might portend for our families and communities.

When policymakers, officials, and experts talk about such threats, they often do so in a language of “value at risk”: a measurement of the financial worth of assets exposed to potential losses in the face of natural hazards. This language is not only descriptive, expressing the extent of the threat, it is also in some ways prescriptive.

Information about value and risk provides a way for us to exert some control, to “tame uncertainty” and, if not precisely predict, at least to plan and prepare prudently for the future. If we know the value at risk, we can take smart steps to protect it.

This logic can, however, break down in practice.

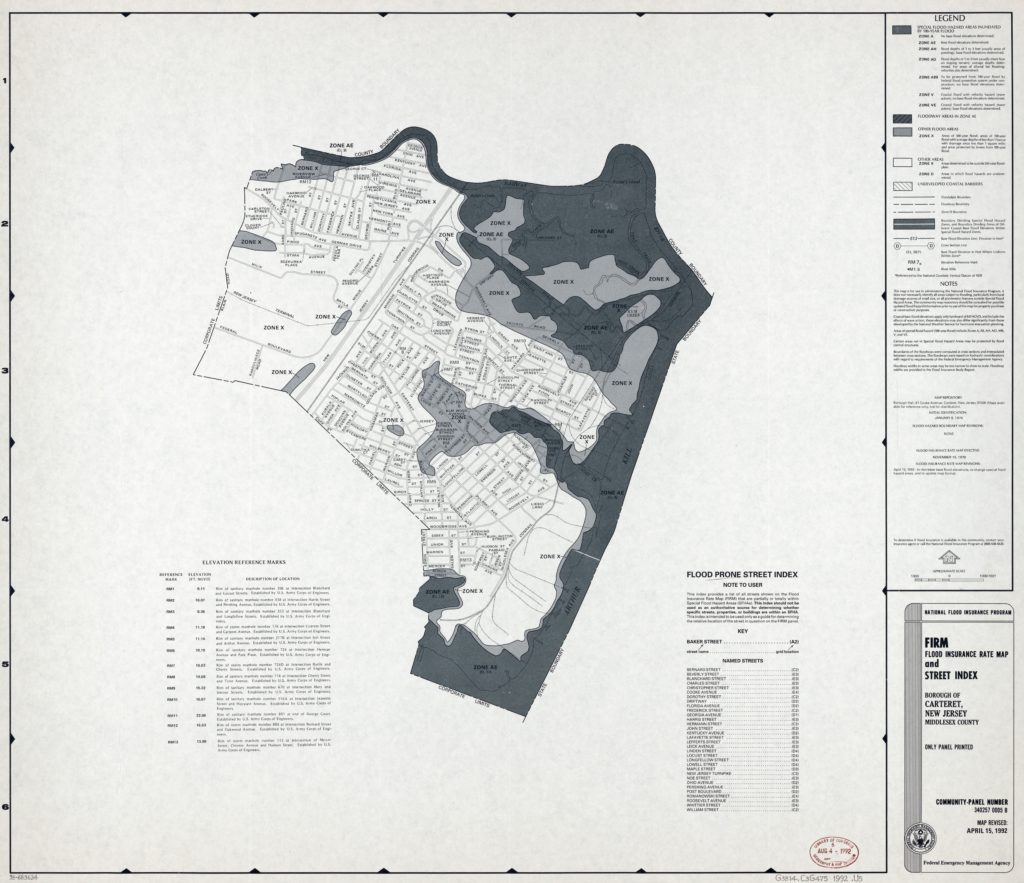

After Hurricane Sandy in 2012, I went to New York City to find out how residents there, particularly homeowners, were responding to a new landscape of “value at risk.” In the wake of the catastrophe, they had received a new “flood insurance rate map” that expanded the boundaries of the city’s high-risk flood zones.

129 billion dollars of property was now officially “at risk” of flood, an increase of more than 120 percent over the previous map.

And yet, I found that many New Yorkers were less worried about the threat of flooding than they were about the flood map itself. As one Rockaway man put it, the map was “scarier than another storm.”

Far from producing clear strategies of action, the map produced ambivalent actors and outcomes. Even when people took steps to reduce their flood risk, they often did not feel that they were better off or more secure for having done so. How can we understand this?

By examining the social life of the flood insurance rate map, talking to its users (affected residents as well as the experts, officials, and professionals who work with them), I found that the stakes on the ground were bigger than just property values and floods. Other kinds of values were threatened here, and not just from floods, complicating the decision of what to do and when.

What is a flood insurance rate map?

The Federal Emergency Management Agency (FEMA) produces flood insurance rate maps to identify and depict the areas of the country at risk of floods. As the name implies, they are used to rate flood insurance, which is provided to homeowners and small businesses across the country through a public, federal program called the National Flood Insurance Program (NFIP). All property owners with mortgages in official high-risk zones are required to purchase flood insurance.

The annual premium is meant to correspond to the risk facing the individual property. Buildings inside the flood zones, especially ones below the expected flood elevations, face higher annual premiums than buildings outside the zones or at higher elevation. In this way, the premium acts as a “price signal” of the underlying risk and should incentivize economically rational, risk-reducing action: elevating the home or relocating out of harm’s way.

Values at risk in New York City

In my interviews and observations in New York City, I found that people generally accepted that they were facing high risk from floods. This is backed up by survey data.

A post-storm survey of homeowners in flood prone areas of New York City found that 86 per cent of respondents believed they lived in a high flood risk area.

But the decision of what to do about it was not a straightforward one of mitigating flood risk. This was because the maps provoked fears about other kinds of risks, unfolding along multiple timelines, that would shape the decision of what to do and when.

For instance, New Yorkers understood the map itself as a source of economic risk. New median premiums for one-to-four family properties in high-risk zones were estimated at $4,200 to $5,600, with some policies going into the tens of thousands of dollars per year.

Many of the residents now facing these new or higher flood insurance premiums were working-class homeowners, for whom risk mitigation would introduce considerable financial strain, even if it would “pay for itself” in savings on flood insurance premiums and avoided flood losses in the future.

One woman, a construction manager in Queens, told me that elevating her home would require her to drain the college savings of her children.

A legal aid lawyer on Staten Island told me her clients were refusing city-provided funds for elevation because they could not afford rent while they were temporarily displaced from their homes. These residents might protect themselves from flood risk but in the process be exposed to economic risks that made them feel less secure.

Yet what made the flood map “scarier than another storm” was not simply about dollars and cents. The new map also threatened the emotional and social values attached to cherished places. It narrated parts of the city as risky, perhaps too risky—and too expensive—for some communities to remain intact.

When I asked Dan in Broad Channel, Queens if the new map might lead him and his neighbors to move, he replied: ‘You’re wasting your breath… we’re never going to move away.’ He described his neighborhood:

“The people who live here are the people who pick up your garbage; they teach your kids; they keep you safe from criminals; and they run into burning buildings. That’s who lives here… There’s a sense of community down here that’s existed since the 20s, and after the storm, this town had the first resource center up, two nights after the storm… We have a sense of community that I think is very strong, and something that is admirable…”

Dan’s neighborhood might not be flood-resilient, but it was socially resilient, a point of pride that made it worthy of defending.

The map, in a sense, stigmatized his community, which he resented and resisted. His attachment to Broad Channel was about more than his financial investment in his home; it was about his emotional and social investments, complicating any rational calculation of the costs—explicit or otherwise—of staying as is, mitigating the risk, or relocating elsewhere.

What can we learn from uncovering values at risk?

The decision of whether, how, or when to respond to changing natural hazard risks cannot be confined to a narrow calculation of property value at risk of flooding, in the way framed by flood insurance and its rate maps. Sensitivity to values at risk, which takes a broader view of both what constitutes “value” and what it might be “at risk” of or from, allows us to better understand these decisions in their real personal and social contexts, which should inform the design of policies and programs oriented to resilient (re)building as we prepare for a climate-changed future.

No Comments